Is inflation used to take out the deficit?

Fixed income market participants are considered more reasonable than equity investors. A bond investor or a bank only wants interest back on the amount lent. Can the debtor pay back, yes, or no? On the other hand, equity investors buy a company that should become the next unicorn in their dreams. This money is, on average, much more risk-averse.

In this weekly trading note from Carlsquare, we elaborate on the following topics, indices, and stocks:

- Is inflation used to take out the deficit?

- Intrerest hike in May 2022 discounted in the market

- The effect of interest developments on stock markets

- Maybe Santa Claus is real after all

- Nasdaq is not yet there

- Can MA50 save Tesla?

- Giants leading the race

- Fed and ECB on the agenda, perhaps EUR/USD can wake up

- Is Santa coming over to Europe?

- OMXS30 at crossroads

- Is it time for the oil price to break resistance

Fixed income market participants are considered more reasonable than equity investors. A bond investor or a bank only wants interest back on the amount lent. Can the debtor pay back, yes, or no? On the other hand, equity investors buy a company that should become the next unicorn in their dreams. This money is, on average, much more risk-averse. So far, it’s easy. To learn about where the market goes, study what bond investors are doing rather than what stock investors prefer.

Then we come to the fact that since the Lehman crash of 2008, central banks have been manipulating interest rates in various ways, most notably by buying back large amounts of bonds. Central banks’ policies have encouraged individuals and investors to borrow more at low-interest rates. You’ve had to move further out on the risk scale to make more money. TINA (“There Is No Alternative”) for institutions managing pension money has meant reducing the weight of bonds (because they gave such poor returns) and instead weighting up the share of equities and real estate etc. The result has been that yield requirement on various assets have fallen almost more than interest rates, with multiple effects on asset prices.

But the focus right now is when rate hikes from the Fed will come and how much. On several occasions in recent years, Fed heads have backed away from rate hike plans for various reasons. However, a rate hike seems quite likely and quite close in time. At least, that’s what the interest rate market discounts.

Interest hike in May 2022 discounted in the market

Below are the probabilities for a rate hike in May 2022. As shown, one week ago, the likelihood of the rate staying in the current interval, 0-0.25 percent, was 52.6 percent. On December 10, this probability had decreased to 42.8 percent – meaning that more than 50 percent in the market anticipate a rate hike in May 2022.

The US yield curve has steepened over the past year. According to expectations, interest rates should rise relatively more at shorter maturities (three to four years), while the flattening at longer maturities is also evident. So far in December 2021, the US five-year Treasury yield has risen from 1.17 to 1.25 percent. The corresponding increase for the 10-year US Treasury yield is more marginal, from 1.46 to 1.48 percent. Bond investors thus expect the Fed to raise policy rates sooner than a year ago. See chart below.

US Government Bond Yields, most recent compared to one month and one year ago

Source: Refinitiv Eikon

Inflation can be a tool to amortize state debt

Interest rates have only moved marginally upwards relative to the current inflation rate. If current inflation and interest rate levels persist, the negative real interest rate will have risen to almost 6% (!) as measured against the US 5-year Treasury bond rate. The counterargument (originating from the Fed) is that today’s inflation is transitory. Evil conspiracy theorists argue that this is a way to inflate away the enormous national debt, something the US has done before in history, for example, in the late 1940s after World War II. If this is the case, investors in fixed-income instruments continue to be big losers.

US Annual Inflation Rate compared to the US 5 Year Government Bond Yield from December 2019 to November 2021

Source: Refinitiv Eikon, www.riksbanken.se

German interest rate expectations have risen somewhat more evenly across maturities than in the US. But the increase is no more significant than the German 30-year government bond barely “coming above water” and yielding a marginally positive rate. The ECB ties interest rates in Europe, leveling the playing field between solid economies in the north and weaker ones in the south.

Germany Government Bond Yields, most recent compared to one month and one year ago

Source: Refinitiv

But that negative interest rates would correspond to low inflation in Germany is certainly no longer valid. Germany, inflation started first in January 2021, compared to Q4 2020 in the United States. Germany’s current negative real interest rate versus 5-year government bonds is about 5.5 percent.

Germany, Annual Inflation Rate compared to the German 5 Year Government Bond Yield from January 2020 to November 2021

Source: Refinitiv Eikon, www.riksbanken.se

The effect of interest developments on stock markets

Investors typically buy growth stocks when interest rates fall, while buying pressure shifts towards cyclical stocks (e.g., industrials) and banks when interest rates rise. The latter companies perform better when interest rates are favorable (which they have not been in continental Europe in recent years).

Growth versus value stocks performance from March 10 to December 10, 2021

Source: Refinitiv Eikon

The graph above illustrates no tendency to shift from growth to value stocks. What might select value stocks is if today’s inflation rate were partially sustained (though perhaps not at today’s high levels, say half - i.e., 3% per annum). The theme would most likely be to get an inflation hedge, and the answer would probably be assets that return safely (without risk of default) for a long time. Investors are likely to end up around non-cyclical consumer goods companies and the like, with stable and relatively predictable earnings levels—possibly also banking and engineering companies. But an inflation hedge can also be gold or real estate.

A worse variant for the stock market would be stagflation, i.e., inflation without the same growth in the economy. Then the stock market will start to perform worse. Let’s hope that scenario doesn’t play out.

Maybe Santa Clause is real after all

Inflation numbers from the US on Friday were in line with expectations. That gave a boost to stocks, and the broader S&P 500 index set a new all-time high. Also, note how MACD just recently passed a weak buy signal. The index is supported from below by a rising EMA9 and MA20. Maybe Santa is real after all.

S&P 500 Index graph from May 5 to December 10, 2021

Source: Refinitiv Eikon and Carlsquare

But is the Grinch found in the weekly chart dressed as the negative divergence between the index and MACD?

S&P 500 index, weekly five-year price graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Nasdaq is not yet there

On Friday, December 10, Nasdaq 100 outperformed the S&P 500 index. But it still has some way left before it could reach a new all-time high.

Nasdaq 100 index graph, from May 5 to December 10, 2021

Source: Refinitiv Eikon and Carlsquare

Note the presence of negative divergence in the weekly chart. Also, note that this negative divergence has been there for quite some time without causing any trouble. One may think that if the Grinch has been lovely so far, why not over Christmas as well.

Nasdaq 100 index, weekly five-year price graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Can MA50 save Tesla?

Tesla has been lagging behind the broader market. The chart below shows that the share is trading in a comprehensive, falling trend channel. Can MA50 save Tesla from falling to the floor?

Tesla share price graph, from May 5 to December 10, 2021

Source: Refinitiv Eikon and Carlsquare

In the weekly chart, Tesla receives support from EMA9. However, the weekly chart shows signs of lost momentum. A break below EMA9 and the 950 USD level may be next.

Tesla, weekly five-year share price graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Giants leading the race

Apple has been leading the race. The share is currently rising exponentially. Another giant is Microsoft that outperformed the market on Friday. The question is whether the giant IT stocks can continue to outperform.

Microsoft share price graph, from May 5 to December 10, 2021

Source: Refinitiv Eikon and Carlsquare

It is nice not having to see the negative divergence for once in the weekly chart.

Microsoft, weekly five-year share price graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Fed and ECB on the agenda, perhaps EUR/USD can wake up

There was no significant volatility in the EUR/USD following Friday’s inflation figures in the United States. This week, both the Fed and ECB are on the agenda on fiscal policy matters. Perhaps this can get some life back to the EUR/USD currency pair trading.

EUR/USD graph from May 5 to December 10, 2021

Source: Refinitiv Eikon and Carlsquare

Mini Future

In the weekly chart, EUR/USD is still at Fibonacci 61.8

EUR/USD, weekly five-year price graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Is Santa coming over to Europe?

The last trading hour was decisive on the New York Stock Exchange. Thus perhaps there is some catch-up to do in early Monday trading. Maybe Santa is done in the US and is now going over to the European stock markets. As can be seen in the chart below, there is quite some distance to the previous high:

DAX index graph, from May 5 to December 10, 2021

Source: Refinitiv Eikon and Carlsquare

MA20 still needs to be retaken in the weekly chart.

DAX index, weekly five-year price graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

OMXS30 at crossroads

The OMXS30 index is bouncing between MA100 and MA50. Which way will it be up or down? Looking at MACD that has recently generated a weak sell signal, the probabilities for up are more favorable.

OMXS30 index graph from May 5 to December 10, 2021

Source: Refinitiv Eikon and Carlsquare

In the weekly chart, momentum is not looking so happy.

OMXS30 index, weekly five-year price graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

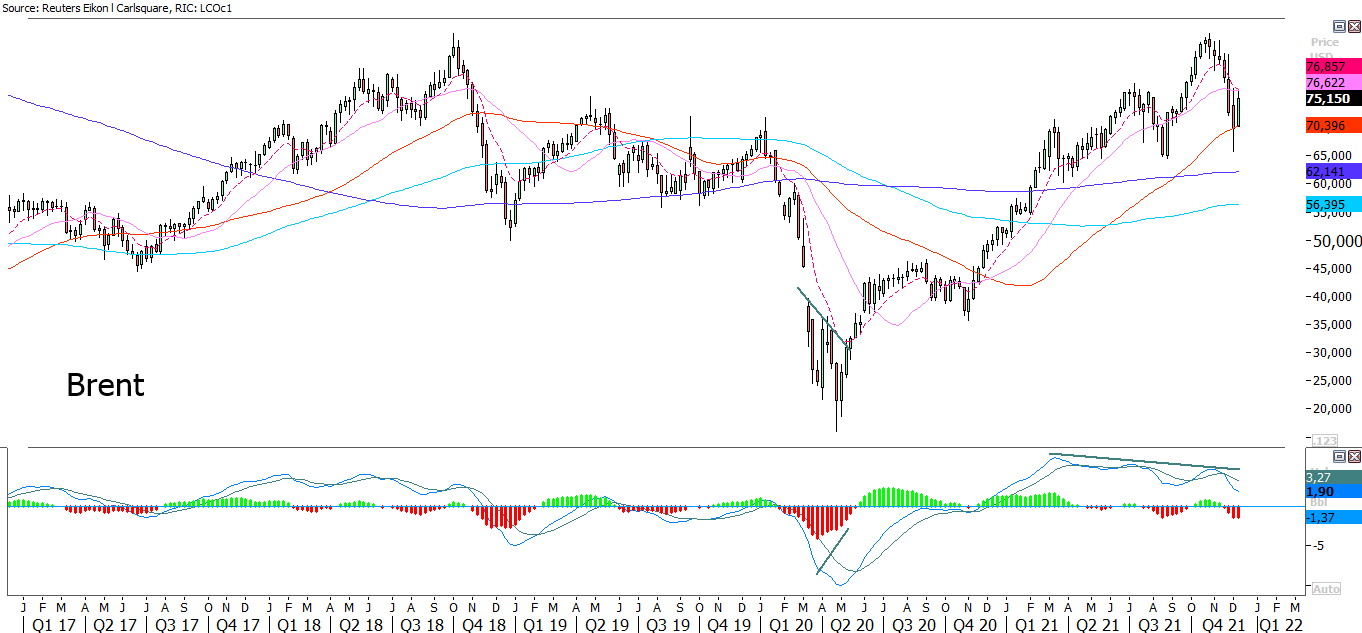

Is it time for the oil price to break resistance

The Brent oil price has retaken MA200 and EMA9, which is now upwards sloping. Next on the upside is the falling MA20 and MA100. In case of a break, MA50 may be next, currently trading just above 80 USD/barrel.

Brent oil price from May 5 to December 10, 2021

Source: Refinitiv Eikon and Carlsquare

MA20 and EMA9 serve as resistance in the weekly chart:

Brent oil price, weekly five-year price graph

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Full name for abbreviations used in previous text:

EMA 9: 9-day exponential moving average

Fibonacci: There are several Fibonacci lines used in technical analysis. Fibonacci numbers are a sequence of numbers in which each successive number is the sum of the two previous numbers.

MA20: 20-day moving average

MA50: 50-day moving average

MA100: 100-day moving average

MA200: 200-day moving average

MACD: Moving average convergence divergence

Risker

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the trading products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms. The base prospectus and final terms constitute the solely binding sales documents for the securities and are available under the product links. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance.