Where are we on the bike?

Several economists have recently called the time ahead of us "the most anticipated recession in history". High inflation, rising interest rates and a general slowdown in the global economy are beginning to make themselves felt, and investors are increasingly using stock market rallies to sell assets rather than buy dips.

Several economists have recently called the

time ahead of us "the most anticipated recession in history". High

inflation, rising interest rates and a general slowdown in the global economy

are beginning to make themselves felt, and investors are increasingly using

stock market rallies to sell assets rather than buy dips.

We are both in a normal position and not. Not,

as in the fact that central banks in recent decades have been able to lower

interest rates to stimulate the economy when needed (with the exception of

Volcker who knew that the economy would suffer great damage at the expense of

fighting inflation), unlike today when Powell, like Volcker, must raise

interest rates into an expected recession. With normal mode, the outlook is

somewhat gloomier. Normal mode, because this type of development was to be

expected because that is what has historically always happened at the end of a

fiat currency's life cycle.

The question we as investors right now need to

answer is thus; where are we on the

bike? And, what bike ?

Before we answer where we are in a cycle, we

first need to define which cycle. If we start by looking at the recession

cycle, it is traditionally described with the following steps:

1. Early in the

cycle: GDP is recovering, economic activity is rising, credit is rising,

profits are growing faster, monetary policy policies are still dove and

stocks are low.

2. The middle

of the cycle: Growth reaches its peak, credit growth remains strong,

profit growth reaches peak levels, monetary policy policies are neutral,

no longer commodity deficits

3. Late in the

cycle: Growth slows, credit tightens, profits fall, tight monetary policy,

stocks grow

4. Recession:

Declining economic activity, more difficult to obtain credit, profits

falling and in some cases going to losses, monetary policy easing and

inventories and sales of inventories falling

Steps one and two are usually described as

recovery, while between the middle and late of the cycle is called expansive

and recession is contractive. Depending on where you are in a recession cycle,

different assets are also attractive to own. With more than a decade of

monetary policy easing and growth behind it, the tech sector looks dark.

Unlike previous recession cycles, we will now

enter a recession with tightening monetary policy. With 14 years of stimulus,

there is no longer room for central banks to hedge interest rates in the event

of declining economic activity. Instead, Powell has been forced into the same

corner that Paul Volcker once was in: destroying the economy to overcome

rampant inflation.

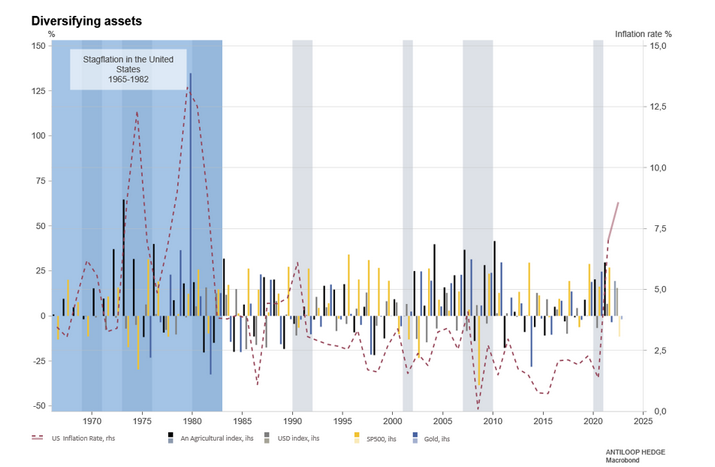

Assets to own during stagflation

The last time the United States was in a stagflatory situation, i.e. a period of high unemployment, high inflation and recession, was between 1965-1982. During that period, assets outperformed gold (only after the US released the gold standard in 1971, however) and agricultural commodities, while the S&P 500 stock index underperformed.

Although history does not promise any guarantees for the future, the probability is greater that the 20s will be similar to the 70s for real assets, which means that for those who believe that we are really heading into a longer period of structurally high inflation and a weaker economy, it is a better idea to own gold than the FAANG companies.

Risks

This information is in the sole responsibility of the guest author

and does not necessarily represent the opinion of Bank Vontobel Europe

AG or any other company of the Vontobel Group. The further development

of the index or a company as well as its share price depends on a large

number of company-, group- and sector-specific as well as economic

factors. When forming his investment decision, each investor must take

into account the risk of price losses. Please note that investing in

these products will not generate ongoing income.

The products are not capitalprotected, in the worst case a total loss

of the invested capital is possible. In the event of insolvency of the

issuer and the guarantor, the investor bears the risk of a total loss of

his investment. In any case, investors should note that past

performance and / or analysts' opinions are no adequate indicator of

future performance. The performance of the underlyings depends on a

variety of economic, entrepreneurial and political factors that should

be taken into account in the formation of a market expectation.

.