This summer's rise is hardly the start of a long-term bull market

Don't fight windmills. They don't care and you will lose no matter what you do. So "Don't fight the Fed". The central banks have decided; inflation must be brought down quickly and resolutely, so the perception that the Fed and ECB have lost control does not take hold. The most important thing now is to counter inflation expectations already at the gate, because once they have been released, it is much more difficult to get them back into the fold.

Don't fight windmills. They don't care and you will lose no matter what you do. So "Don't fight the Fed". The central banks have decided; inflation must be brought down quickly and resolutely, so the perception that the Fed and ECB have lost control does not take hold. The most important thing now is to counter inflation expectations already at the gate, because once they have been released, it is much more difficult to get them back into the fold.

It is easy to lose perspective when following the daily market movements. Not least when a reflexive summer rally lifts the Nasdaq by 25%, which corresponds to two to three full annual returns. Then it can feel as if the boom times are back. But if you zoom out a little to get a better overview, you will see that the negative stock market trend has not been broken. Not even after the ongoing secondary bear rally that began just over a week ago. On the contrary, it just looks like a classic body fin of the market, but without breaking up through any important levels.

But above all, it is the Fed that holds the stock market's pace now, and there you quickly see that CPI inflation remains at 8% in the US and 9% in Europe, which means that the Fed's interest rate increase plans remain. The Fed has never ended a rate hike cycle until the rate is higher than CPI inflation. Maybe they meet around 4-5% in a few years. The fed funds rate will thus rise by another 1.5-2 percentage points, to the end station of around 4-4.5% in six months.

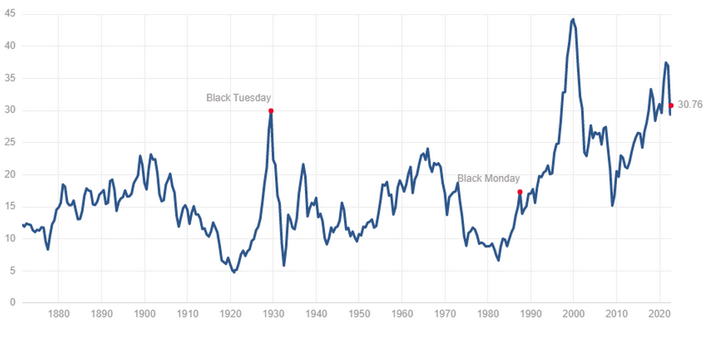

US Consumer Price Index (CPI) in %

In the meantime,

Quantitative Tightening is also beginning to bite seriously in the financial

markets. So far, the economy has not actually been affected by the higher

interest rates. Too little time has passed. Increased interest rates have their

greatest effect in the 12-18 month horizon. On the contrary, the third quarter

seems to look relatively positive, especially in the US where price rises

(which have a positive wealth effect) and written off student loans as well as

high nominal wages all work together for a good quarter. However, this only

means that the Fed holds the tightening line all the more firmly.

The bear rally that

began in mid-June was most likely based on the fact that the decline in the

first half of the year was historically extreme, as well as on the fact that

the third quarter could show a slightly better economy. But when the Q3 reports

are presented, the conditions are instead the opposite. Then you look ahead to

a much weaker Q4 and 2023 because the increased interest rates in 2022

ultimately have an effect on both reported results and not least the

expectations for the coming year. This is happening at the same time as looking

back at a very strong stock market rise June-September and therefore has quite

a lot of fall potential just to get down to the situation that applied at the

beginning of the summer.

To summarize the

situation, inflation is extremely high from a historical perspective. This

means that the central banks resort to historically extreme measures by the Fed

raising the interest rate by 400-450 points in a short period of time and at

the same time both ending QE and starting QT (quantitative tightening). There

is no reason for the Fed to suspend this as long as there are plenty of job

postings out there and low unemployment.

On the contrary, the Fed wants to cause a mild recession because it is the only reliable way to quickly overcome inflationary pressures. Stock market valuations are still far higher than historical normal levels if measured by cyclically reliable key figures such as Price-to-Sales (P/S) and Market Cap/GDP or Shiller Price/Earnings (P/E) or Hussman MAPE ratios. So we still have an expensive stock market, just up 25%, facing extreme monetary tightening and a likely recession. This is happening at the same time as we have increasing geopolitical tensions in the form of Russia-Ukraine and China-Taiwan-US, not to mention a potential energy crisis this winter because of it. These are conditions designed for the bear market that has started to take its completely normal second big step down.

Of course, everything does not have to fall out of control in such a scenario. Low multiple companies in the energy sector and mineral extraction, and perhaps also retail banks can actually benefit in absolute terms from inflation, rising interest rates and the energy crisis, but at the same time it means worse times for those who have to pay for the energy and the increased interest rates. In addition, the abundance of cloud-based admin software that is operated with negative cash flow and valued at extremely high sales multiples will continue to decimate the stock market.

A few times sales is perfectly fine for the best companies that are likely to emerge stronger from the purge, but 10 times sales for all sorts of SaaS companies and other pandemic hype companies is still at least twice as much as justified. The higher the interest rate goes and the recession shows itself to be serious, the more these can be affected by both reduced forecasts and increased yield requirements. Then further price halvings for companies such as Snowflake, Cloudflare, Bill.com, Lululemon, Shopify and Netflix could be more than justified.

On the buy side, however, you probably have to be a little more careful with what you choose, because there are few stocks that are usually spared when the panic pulls the correlations to one. But the big oil companies COP, CVX, OXY, and the big Nordic banks Danske, Swedbank and SHB, are well situated. Maybe you actually dare to add some classic producers of cheap small cars as well, such as Renault, Stellantis and Honda, as they have already been pressured by the Ukraine war and higher fuel prices. This applies in particular to the mother of hype companies: Tesla.

Gold mines such as NEM

and AEM could also be able to get a new push upwards, but it may also be some

time before you actually believe that the Fed will pivot to lower interest

rates. Gold has generally been a disappointment in the past year as neither war

nor inflation has managed to lift the price.

Semiconductor

companies that I have long believed in, e.g. Intel, Applied Materials and

Micron, unfortunately still look very sluggish - and in a recession, continued

oversupply can unfortunately push prices even more, despite already very low

multiples. On the other hand, it is in any case a better bet to bet on these

'real' products at single-digit P/E ratios than SaaS (Software as a Service) companies

with unclear justification for existence at P/S ratio>10.

The outlook for autumn and winter is very negative in my book, but there are good opportunities to hide or even ride well on investments in selected sectors and companies, so you are ready with fresh cash when the stock market hopefully turns up again sometime in 2023 when one dares to hope for a Fed-induced 2024 presidential election rally.

Bull & Bear-Certificates

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.