The US shuts down. Markets fall with the economy and gives the Fed the finger

We have previously pointed out the bullish falling wedge and the positive divergence between the index and MACD, which is a nice set-up for a technical bounce. This technical bounce also came, but it was short-lived when reality hit investors.

The stock exchanges were set for a technical recoil last Friday:

We have previously pointed out the bullish falling wedge and the positive divergence between the index and MACD, which is a nice set-up for a technical bounce. This technical bounce also came, but it was short-lived when reality hit investors. The corona virus causes country after country to shut down and lock their residents into more or less voluntary home quarantine.

There are strict guidelines set up in Norway. There it is still OK to go out shopping and have contact with those you live with if you are healthy. But most other activities are banned - except to go hiking, which is only banned for the infected. Note also that it is not allowed to stay in the cottage, which is an extrem intervention for the Norwegians.

In Sweden, we are increasingly leaning towards the fact that all these measures (that for example Norway has imposed) are not in proportion to the disease. Hopefully, countries in general will expand their healthcare capacity in the coming weeks, but for the global real economy, this is a catastrophe. There are no figures showing the impact yet, but Goldman Sachs estimates the impact on the GDP in the United States at minus 24 percent. Unfortunately, we are inclined to believe that they are on the right track.

Shipping from the world's ports is now declining rapidly. Blow is a comparison for Shanghai and Yangshan port calls in China 2020 versus 2019:

The picture below shows electricity production in China that has been falling sharply over the past three months. Had each month been reported separately, the decline would surely have been considerably more severe.

Although Chinese authorities claim that they have overcome the spread of infection, we do not think the wheels have started spinning in China again. We get reports from the telecom operators that the internet networks are getting choppy due to increased traffic, while we hear from the telecom providers that they are getting lots of orders for new equipment. But they are not able to deliver as their factories are at a standstill mode. The same applies to for example installers who cannot get into closed factories and do their maintenance work.

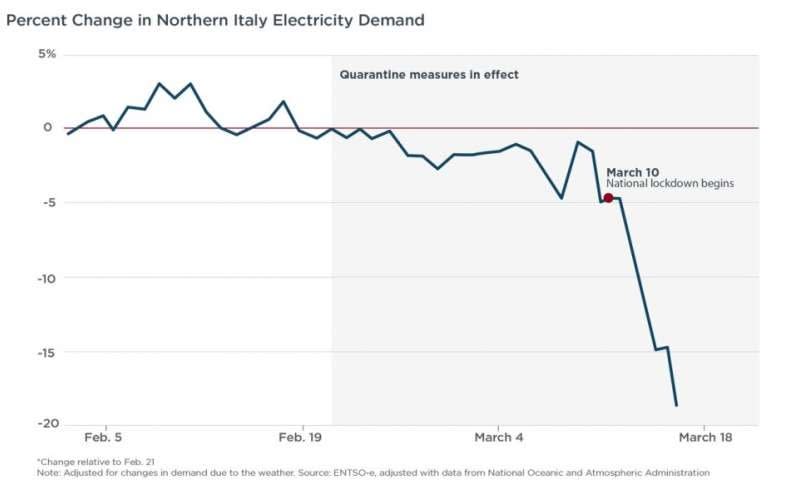

In Italy, electricity consumption looks as below:

This is a decrease of 20 percent and is in a continued fall. This can be a good forecast for the entire economy. In the United States, the unrest is most visible in individual equities as insurance companies that face enormous claims for damages. AIG will of course refer to Force Majeure, but the costs will still be huge.

The market for high risk bonds remains our best indicator of the true risk appetite in the market. Below it is risk appetite reflected in the ETF for junk bonds, HYG. Note that HYG is at a free fall under high volatility:

This implies that the market is now expecting a tsunami wave of bankruptcies. Not until this graph flattens out, do we believe in a real upturn in either the real economy or the stock exchanges will occur.

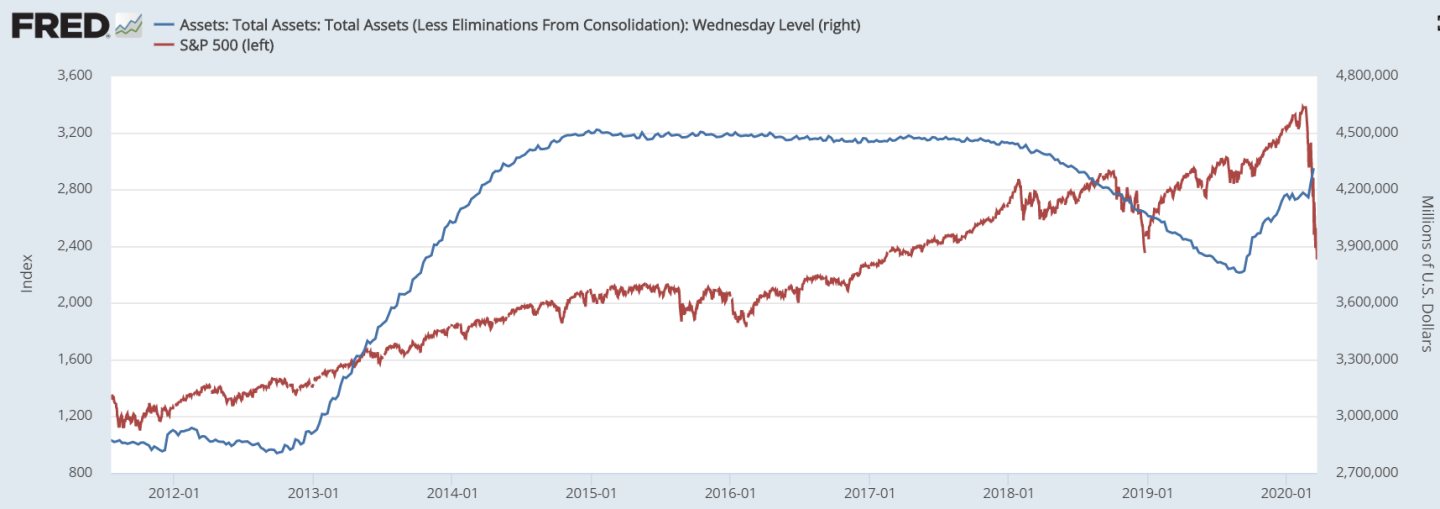

The Fed is now doing its best to mitigate the decline. The red line in the graph below shows the rise and fall of the S&P 500 index. The blue line shows Fed support purchases that are now gaining momentum soon to be over and past the previous peak.

But this does obviously not dampen the decline in the stock market, which shows that investors have lost confidence in the Fed. The axiom "don’t fight the Fed" seems to be wrong this time. There are two explanations for this. One is that the Fed's actions are too small but, above all, are misplayed. G7 or G20-level actions are needed to surprise the market. The lack of coordination between the countries is obvious.

Now Saudi Arabia, which has the presidency, has called for a G20 meeting this week. It will be held on video. Attending the meeting will be finance ministers, governors of central banks and leaders of health, trade and foreign ministries. If they are skilled, they will prepare for a joint action. One example of such action would be that Saudi Arabia and Russia could shake hands on a new oil production cap. We believe that massive sales of equities and bonds from the oil countries are a contributing factor to the rapid fall. If you want to burn funds that have gone short in the market, they can also add to the action plan to let the central banks to directly buy shares in the market.

However, the single biggest action to be made is to rectify the rapid rise in the USD. A more expensive USD hits hard on all emerging economies, which as an effect have a more challenging time to find financing and get to pay more expensive interest rates and loan repayments. After all, it is a matter of time before countries start to go bankrupt, such as during the Greece crisis. Italy is almost at hand right now, although the situation for Spain is almost as bad.

Below shows the daily graph for the USD:

In order to find the next level on the downside, you need to go back to 2016/2017 where the 1.05-level can be identified:

But the G20 countries cannot do anything about the real economy. The only thing that can have a positive impact on this time is that a vaccine is coming out or that countries are deliberately releasing the draconian measures that have been introduced.

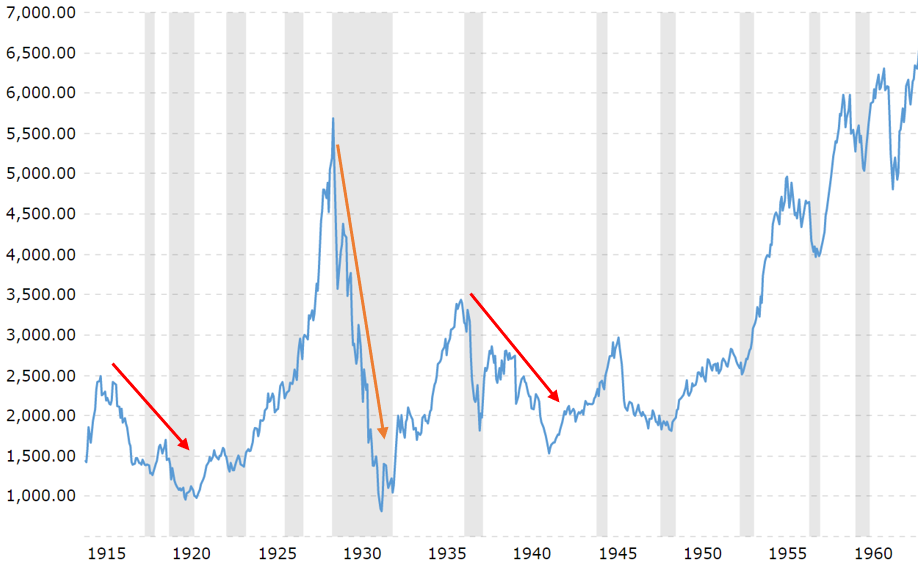

The graph below shows the Dow Jones index in the United States. Right now, everyone compares this situation to the 1929 crash, which can be right from many perspectives. See the orange arrow below. But there were two stages in that crash. The first phase was the financial downturn. The second phase was the real downturn for the economy:

The first phase can best be illustrated when the graphs for this situation (blue) are laid above the graph from 1929 (red):

The first phase of the downturn is about as fast today as it was in 1929. Then in 1929 came an upturn in the index, followed by a murderous slow recession between 1930 and 1932. This second recession was probably due to the US tightening its liquidity at that time, which lowered the entire real economy. It is these incorrect actions that former Fed chief Ben Bernanke was particularly interested in.

It is this second phase of the decline that we must do everything possible to avoid right now. After all, this crisis is worse than the 1998 Asian crisis, the IT crash in 2000 and the Lehman crash in 2008, which affected only parts of the economy. The 2020 crash cannot be escaped from, it affects us all.

The other two red arrows in the graph above (with the orange arrow) for Dow Jones show the market reaction to the World War I and the World War II. Probably it is these periods that it is correct to compare with now. We are not talking about a third world war but closing cities and entire countries has the same effect as a war have on the economy. Before these closures of cities and countries are lifted, there is no need to rush into the stock exchange. On the contrary, liquidity is everything right now. The risk is imminent that we end up with super-fast growth in unemployment rate and deflation, which can give a rapidly falling spiral to the world economy.

We believe this is an insight that will spread in the coming weeks. Hopefully, the production capacities will be redeployed quickly so that the hospitals get the material they need, and more medical facilities can be set up. In this way, relief can gradually be introduced and dampen the fall in GDP. Sooner or later we will come out of this crisis too.

Even though we sound slightly gloomy this time, there are always upsides even in downturns and downturns are always followed by upturns. Note the persistent ascent phase that began in the 1950s when all the wheels of the world began to spin again (see graph with orange arrow above).

In the quarterly graph for S&P 500 below, one can see how the long-term rising trend is broken:

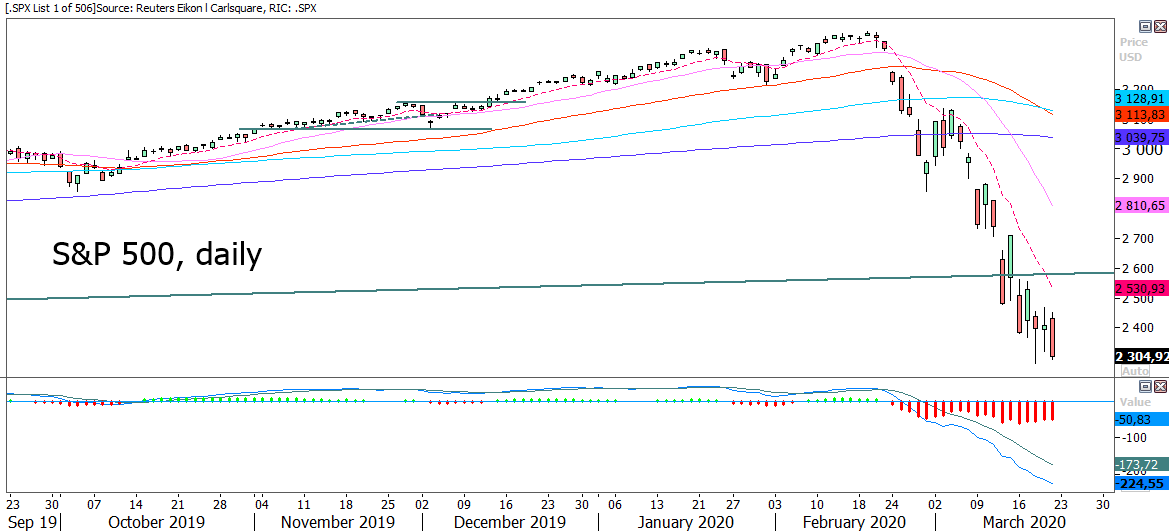

The weekly graph for the S&P 500 below shows that the steep fall so far has broken through all levels of support:

Note that the index is trading at 2305. President Trump was elected at the level of 2083. Therefore, both even 2200 and 2083 will be strong levels of support.

But in this type of market you must take a day at a time. There are no signs of reversal in the daily graph:

Mini Futures

In the monthly graph below, Nasdaq is balancing on support in form of a rising trendline:

Mini Futures

The Tesla share has bounced nicely on MA200 in the daily graph below. However, a falling EMA9 around USD 490 is pushing downwards from above and MACD is showing no sign of recovery:

The next level on the downside can be found right above the USD 285-level.

Bull & Bear-Certificates

For OMXS30 index, the long-term rising trend has been broken as visualized in the quarterly graph below. Some sort of support can be found between 1262 and 1235:

In the 30-minute graph below one can see how the index is trading close to the floor of a short rising trend. The first level of support on the downside can be found around 1262:

Mini Futures

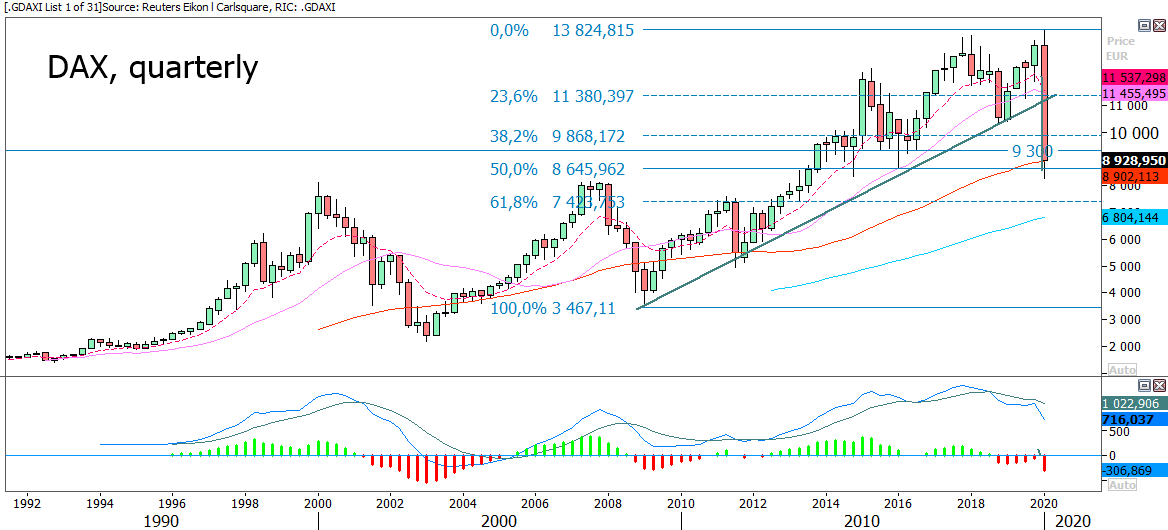

The DAX index is also trading below the long rising trend in the quarterly graph below:

In the 30-minute graph below, one can see how DAX gapped up on Friday. The first level of support on the downside can be found around 8 645 followed by 8 265:

Mini Futures

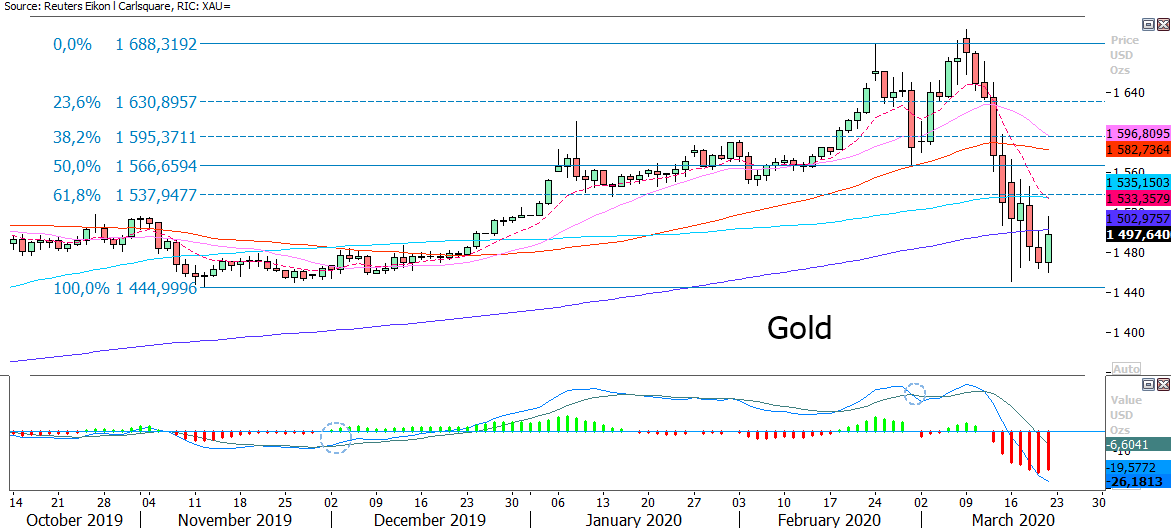

When everything is for sale, even gold is sold off. Note how gold is trading below MA200. The next level of support can be found around 1445:

Mini Futures

Bitcoin is also having a rough time during times like these. Bitcoin in its weekly graph below is trading at a support level in the form of a rising MA200:

Support can be found at the 4 000-level followed by 3 047.

Risks

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.