Summer days…are here to stay!

There is always something special about the summer markets. They are usually tough and sleepy. The big names in the markets are on holiday and the trading desks are filled with juniors who are reluctant to make their own decisions. A short summary is that if everything is as it should be, the markets will slow down.

There is always something special about the summer markets. They are usually tough and sleepy. The big names in the markets are on holiday and the trading desks are filled with juniors who are reluctant to make their own decisions. A short summary is that if everything is as it should be, the markets will slow down. But if the thunderstorm breaks out, the initial negative reaction will be all the greater. It is no wonder that the options market is showing two faces right now. US volatility index VIX tests the multi-year lowest, but the SKEW index (details on the SKEW index below) shows that put options are significantly more expensive than call options. This indicates that there is a willingness to pay extra for protection now that summer substitutes are taking over.

What we saw two weeks ago was how the Fed throw up some test balloons to see how the market would react to the Fed starting to reduce subsidies and raise interest rates. As expected, this created unrest in the market with falling stock prices and a rising USD. The only market that went unaffected out of this was the fixed income market…!

Either or, it is exceptional professional to see through Fed´s manouvers, or the Fed holds the market in a tight grip and controls it with a firm hand.

The interest rates in the form of the 10-year US government bond yield have made a nice landing around 1.5 percent. Note that the interest rate in the US rose by 3.3 percent on Friday 25 June (percent, not percentage points). This came after an unusually high inflation figure of 3.9 percent in the United States. See graph below:

US 10-year government bond yield graph from January to June 2021

US 10-year government bond yield, five years weekly graph

Note: Past performance is not a reliable indicator of future results.

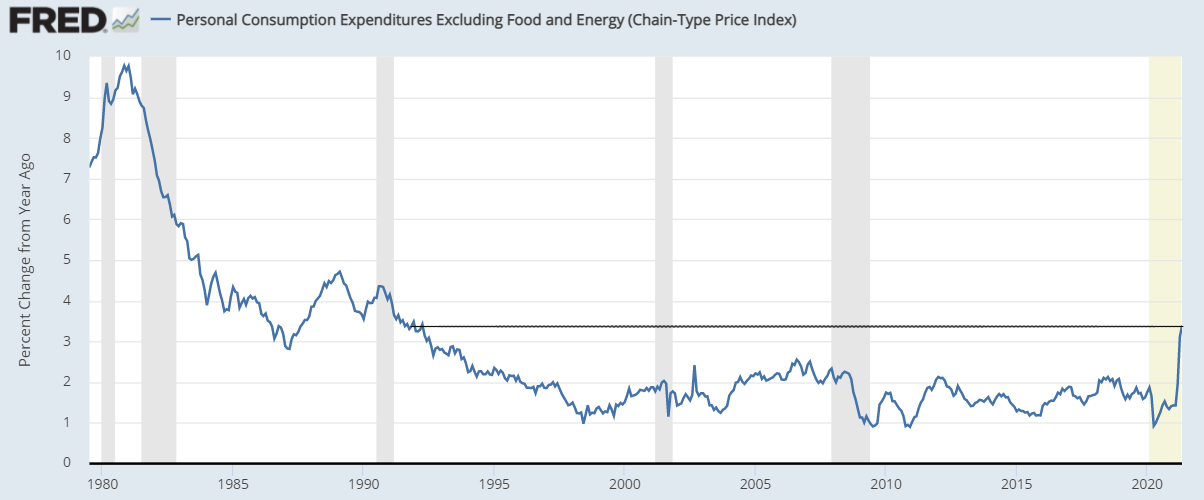

Seen in perspective above, one must go back to the 1990s to find an equally high inflation figure in the United States. But the market is currently expecting such figures since there is a shortage of specific goods due to Covid 19. Had 3.9 percent arrived without a warning, the reaction would have been panic. Now the market still expects inflation to be transient.

US Personal Consumption Expenditures excluding Food and Energy from 1980 to 2021

Note: Past performance is not a reliable indicator of future results.

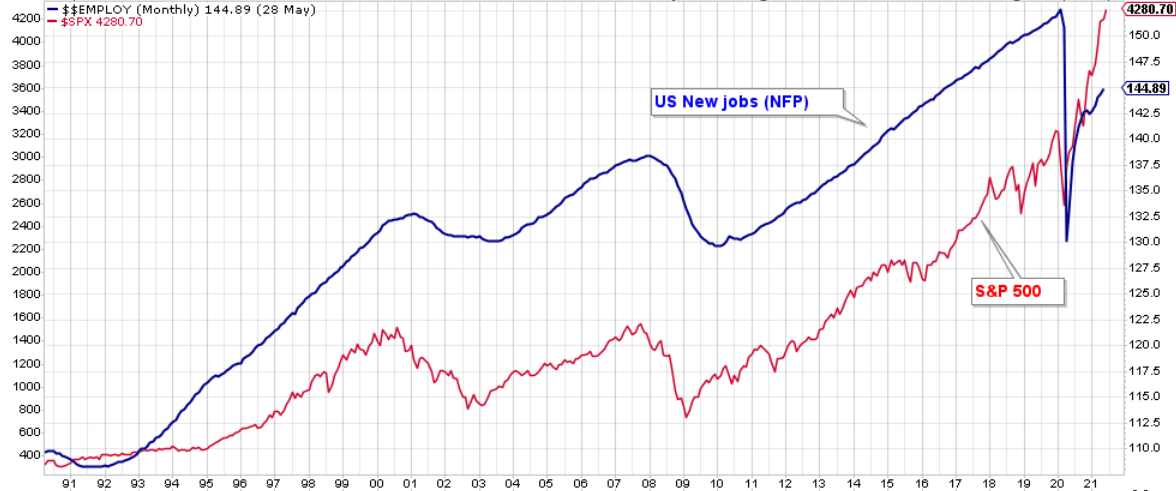

Instead, the focus is on Friday's (July 2) job figures for June in the United States. Will it be another weak month where the workforce prefers to be at home with subsidies instead of dragging shopping carts at Wal-Mart or flipping burgers at McDonalds? The large subsidies for the unemployed expire in September. If they are not extended, it can create a lot of social unrest…These are decisions that must be made by August. At the end of August, it is also time for the annual central bank meeting in Jackson Hole, August 26-28. This is when the markets expect the Fed to provide clearer information on what is expected in the coming years in terms of interest rate developments. What we have seen so far is just test balloons… The sharp downturn followed by a rapid rise again shows that a downturn should be bought in this market. The central banks have no intention of giving up support purchases or reducing their own power.

S&P500 index (in USD) performance compared to new jobs being created in the United States from 1991 to 2021

Note: Past performance is not a reliable indicator of future results.

If you look at the S&P500 index price performance between the years 1993 to 2012, it turns out that July is the worst month of the year and that the autumn is normally strong.

Percentage of months in which S&P500 index closed higher than it opened from 1993 to 2012

Note: Past performance is not a reliable indicator of future results.

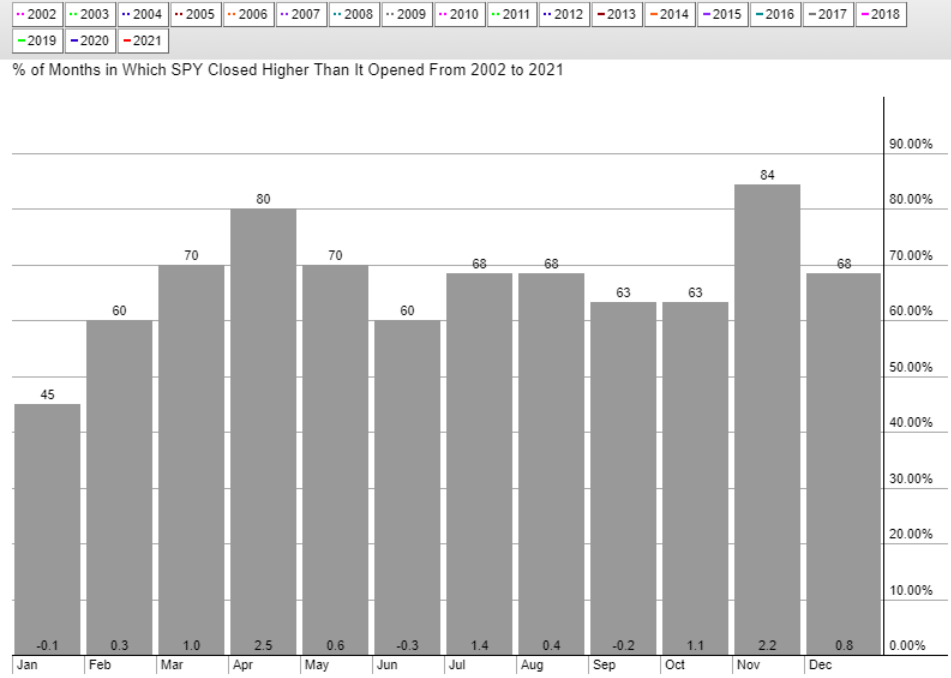

If you scroll forward in the time from 2002 to 2021, this pattern is erased. The summer months are stable. But it is also clear that the big upswings occur in the spring and autumn.

Percentage of months in which S&P500 index closed higher than it opened from 2002 to 2021

Note: Past performance is not a reliable indicator of future results.

So how to interpret this?

When you go into individual years, there are a few years that are outliers. It is mainly 2013, 2014, 2015 and 2019. All these years had clear declines, during the summer months (see below). But every year it recovered. Except for one year: 2015.

Performance of the S&P500 index from 2012 to 2021

Note: Past performance is not a reliable indicator of future results.

This is how CNN Business wrote about 2015 in its autumn column:

The new year could not come soon enough for many investors.

US markets finished 2015 mostly in the red: The Dow was down 2.2 percent. The S&P 500 ended the year down 0.7 percent. It was the worst year for those two indices since markets collapsed 2008.

(…) Volatility trashed investors left and right in 2015. The three big concerns this year were falling oil prices, China's economic slowdown and the seemingly never-ending speculation about when the Federal Reserve would raise interest rates.

Greece's debt crisis, the European Central Bank's stimulus plan and fears of a broader slowdown in emerging markets kept investors on their toes too.

Note that the oil price fell, and that the Greek crisis was ongoing. Otherwise, it is a pretty good description of 2021!

The Federal Reserve's balance sheet expansion from 2009 to 2021

Note: Past performance is not a reliable indicator of future results.

But there is a big difference and that is the Fed´s support purchases. 2013 was a troubled year because then tapering would take place for the first time, which ended with renewed support purchases. From 2014 to 2020, the Fed remained at previous levels. It is only with Covid-19 that financial support has exploded. Our conclusion is that unless there are external shocks such as the Greek crisis, S&P warning of the US mountain of debts (2011) or pandemics such as Covid-19, the summer months are now rather pleasant stock market months.

If Nike in any way is an indicator for the upcoming Q2 2021 reporting season in the USA, it is likely to be strong. Nike shares rose by 15.5 percent on their interim report on Friday 25 June, where the management presented a positive forecast for 2022.

Nike share price graph (in USD)

Note: Past performance is not a reliable indicator of future results.

Nike five-year weekly graph (in USD)

Note: Past performance is not a reliable indicator of future results.

FedEx’s interim results came in just above expectations, but the share still fell. This indicates that the market had discounted a higher than officially anticipated EPS.

Fedex share price graph (in USD)

Note: Past performance is not a reliable indicator of future results.

Fedex five-year weekly graph (in USD)

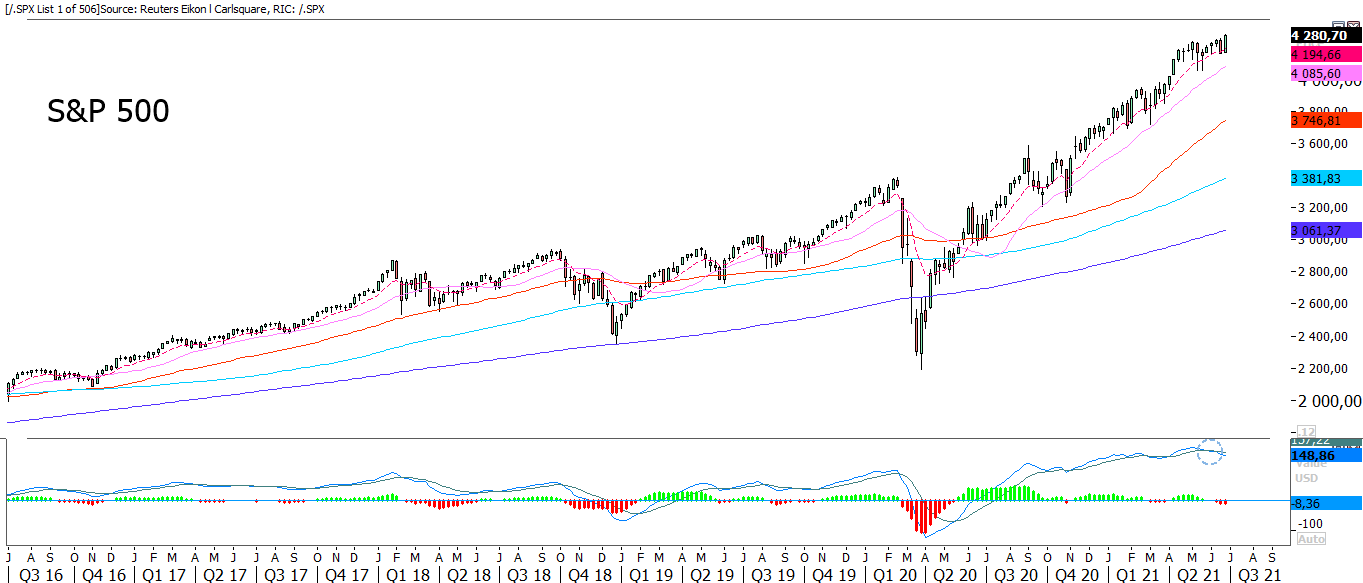

The S&P500 index bounced on the moving average MA50 when the Fed released balloons but is back at a new all-time-high. Yet another all-time-high was set on Friday 25 June. Also note that MACD (moving average convergance divergance) now has generated a weak buy signal.

S&P 500 index graph from October 2020 to June 2021 (in USD)

Note: Past performance is not a reliable indicator of future results.

S&P 500 five-year weekly graph (in USD)

Note: Past performance is not a reliable indicator of future results.

The market for junk bonds shows continued high risk appetite. See graphs below for iShares Iboxx high corporate yield bond (HYG) ETF:

HYG ETF price graph from January to June 2021 (in USD)

Note: Past performance is not a reliable indicator of future results.

HYG ETF five-year weekly graph

Note: Past performance is not a reliable indicator of future results.

Tech companies are again revived engines for the markets. However, tech-heavy Nasdaq 100 index did not manage to continue its upwards movement after Thursday’s gap (24 June). Is a closing of the gap in the cards?

Nasdaq 100 index price graph from October 2020 to June 2021 (in USD)

Nasdaq 5-years weekly graph (in USD)

The FANG (Facebook, Amazon, Netflix, Google/Alphabet) company stocks that have also been drivers of the market has shown signs of weakness during the last two trading days.

Below is Amazon that did not manage to set a new all-time-high…this time. On Friday 25 June, the share also closed below exponential moving average EMA9. Will the stock manage to give it another try this week? Perhaps MA20 should be tested first?

Amazon share price graph from October 2020 to June 2021 (in USD)

Note: Past performance is not a reliable indicator of future results.

In the five-year weekly graph below, one can see how momentum is once again rising:

Amazon share five-year weekly price graph (in USD)

Note: Past performance is not a reliable indicator of future results.

Bull & Bear-Certificates

Facebook shares also fell on Friday after setting a new all-time-high on Thursday 24 June. Nevertheless, the trend is still strong as both EMA9 and MA20 is still rising:

Facebook share price graph from October 2020 to June 2021 (in USD)

Note: Past performance is not a reliable indicator of future results.

However, in the weekly five-year graph below, one can see how RSI is overbought. Nevertheless, this is not a sell signal stand alone.

Facebook share five-year weekly price graph (in USD)

Note: Past performance is not a reliable indicator of future results.

The US volatility VIX index, which shows the market´s pricing of expected volatility over the next 30 days, is down to year-low levels. It pays to buy VIX when it tests the lower Bollinger Belt, which is currently happening intraday.

VIX price graph from February to June 2021

Note: Past performance is not a reliable indicator of future results.

VIX five-year weekly price graph

Note: Past performance is not a reliable indicator of future results.

However, the Skew index gives yet another signal from the option market. Skew shows the pricing differences of downside options (simplified as put options) in relation to at-the-money options or upside options (simplified as call options) in terms of implied volatility. The higher the Skew index, the more expensive it is to buy protection through put options and vice versa. However, last week the Skew-index spiked to close at 170.6. That is a level never been seen before. It implies that pretty much no one wants to sell put options with an expiry within the next 30 days…so even though VIX implies a calm summer – nobody wants to sell you protection against a potential fall.

Skew index five-year weekly price graph

Note: Past performance is not a reliable indicator of future results.

Another important factor for US stocks is the USD. A weaker USD function as fuel for US stock and vice versa. The USD (dollar-index) has slipped on the MA200. If we were the Fed, we would keep interest rates and the USD on the leash – everything else takes care of itself as long as these two forces are kept under control.

Dollar-index (USD) performance graph from November 2020 to June 2021

Note: Past performance is not a reliable indicator of future results.

Dollar-index (USD) five-year weekly price graph

Note: Past performance is not a reliable indicator of future results.

Euro has the highest weight in the currency basket that the USD is traded against in the Dollar-index. The EUR/USD is thus looking close to an inverted Dollar-index. As shown in the graph below, the currency pair is consolidating just below Fibonacci 38.2 as well as EMA9. In case of a break to the upside, resistance can be found between 1.199 and 1.203.

EUR/USD graph from October 2020 to June 2021

Note: Past performance is not a reliable indicator of future results.

Mini Futures

EUR/USD five-year weekly graph

Note: Past performance is not a reliable indicator of future results.

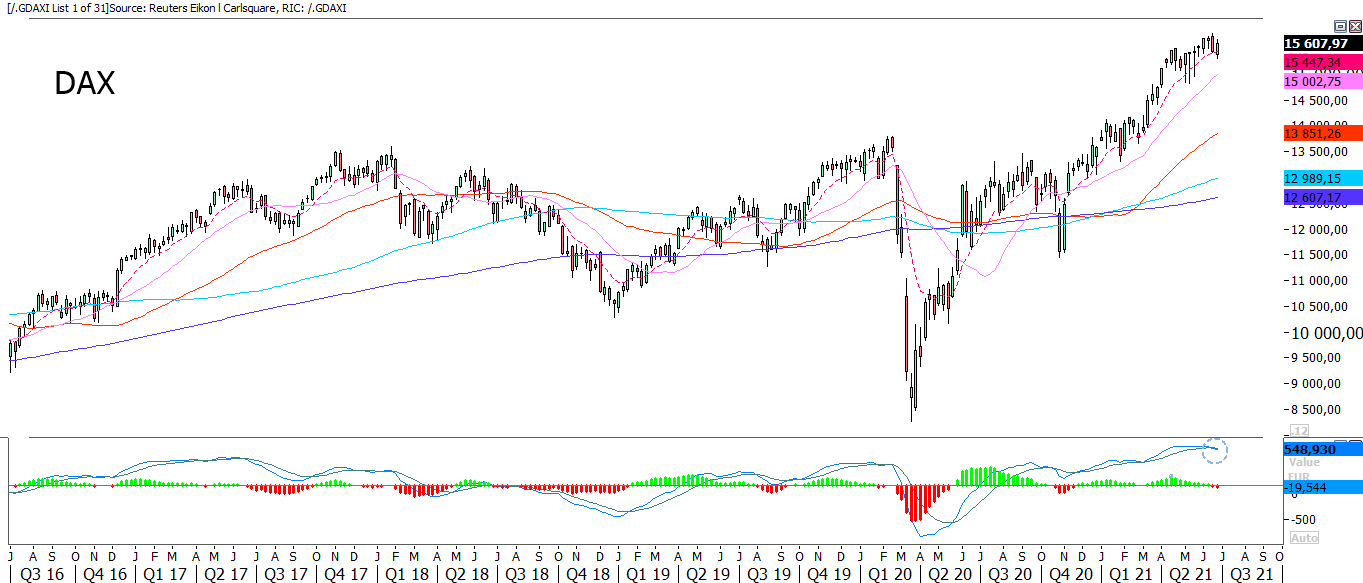

Shown in the graph below, the German DAX index bounced like S&P 500 on MA50 but is having difficulties to break above a falling EMA9. Keep an eye on the EUR/USD. Unlike US shares, German stocks typically gain from a decline in EUR/USD.

The DAX index graph from December 2020 to June 2021 (in EUR)

Note: Past performance is not a reliable indicator of future results.

The DAX index five-year weekly price graph (in EUR)

Note: Past performance is not a reliable indicator of future results.

The Swedish OMXS30 index is less exposed to tech and growth stocks (compared to S&P 500 and Nasdaq) and is thus also facing challenges. MA50 still holds but momentum is falling. In case of a break on the downside, MA100 currently trading close to 2 180 may be the next level:

The OMXS30 index from October 2020 to June 2021

Note: Past performance is not a reliable indicator of future results.

OMXS30 index five-year weekly price graph

Note: Past performance is not a reliable indicator of future results.

Gold is also exposed to movements in USD. The correlation is high, and gold is just like the USD consolidating. A weaker USD is good news for gold and vice versa.

Gold price graph from October 2020 to June 2021 (in USD)

Note: Past performance is not a reliable indicator of future results.

Gold five-year weekly price graph (in USD)

Note: Past performance is not a reliable indicator of future results.

We are now taking summer vacation but will be back in August. Have a nice summer and keep an eye on the graphs!

Full name for abbreviations used in previous text:

EMA 9: 9-day exponential moving average

Fibonacci: There are several Fibonacci lines used in technical analysis. Fibonacci numbers are a sequence of numbers in which each successive number is the sum of the two previous numbers.

MA20: 20-day moving average

MA50: 50-day moving average

MACD: Moving average convergence divergence

Risks

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the trading products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms. The base prospectus and final terms constitute the solely binding sales documents for the securities and are available under the product links. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance.