It's springtime for precious metals

Since the peak in August last year, gold, despite massive monetary policy stimuli, has had a tough time. It has been speculated whether it has been Bitcoin's upside that has led the gold price to fall from peak levels of $ 2069 in early August to below $ 1700 in late March, or whether it has simply been too attractive for investors to invest. in risk-on-assets during the same period.

Bull & Bear-Certificates

In the last six weeks, however, the trend has reversed for the historically inflation-proof precious metal. Since the bottom on March 30, the price of gold has risen by almost 11 percent, and the conditions for further upside during the year have rarely looked better.

There is a general skepticism towards investing in commodities among private investors. For those who are used to investing in shares, the counter-argument against gold is usually that gold according to Warren Buffett would have overpriced shares, and that it is thus a bad investment, and of course, that the yellow stone does not produce anything and thus does not create a value.

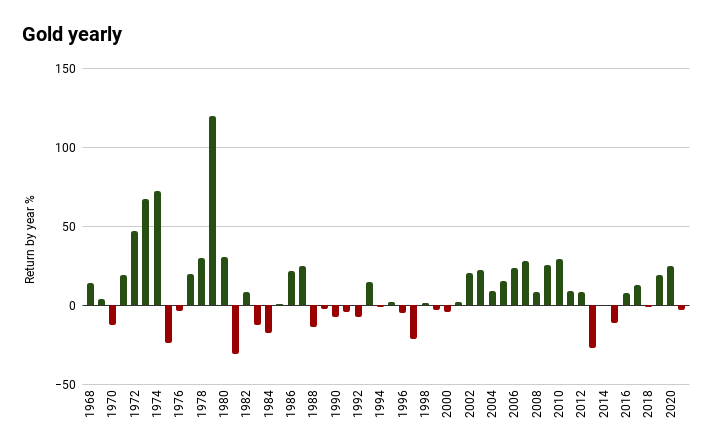

If you go back to 1968 and look at how the gold price has performed annually since then, we can state that the average return has been 10.3 percent. In other words, it is higher than what the large-cap index S&P 500 returned on average during the same period.

However, it is very important to remember that it is not about choosing the "right asset" and then keeping it forever. Without the best risk-adjusted return being achieved through a diversified portfolio with a low correlating asset class, something for which Harry Markowitz, the creator of Modern Portfolio Theory, received the Nobel Prize in the 1950s.

No asset should make up 100 percent of a portfolio, but each part should work in interaction with the others. Under different market conditions, different types of assets work differently, and that is precisely why, depending on the prevailing climate, you want to be able to adjust the allocation in your portfolio. Gold and precious metals (along with other commodities in general) tend to do better during periods of high inflation, something we saw during the 1970s, among other things. At the same time, share prices and valuations tend to fall during the same period, which makes commodities an attractive alternative to then be able to sell off to buy shares at lower prices.

However, the ultimate goal should be to try to own as much producing assets as possible measured over long periods of time. This means that precious metals and raw materials should generally be used as tools to give investors the opportunity to buy shares at a lower price.

For the past twelve to thirteen years, the climate has been perfect for equities, but now the trend has reversed. High inflation is already a fact and the price of commodities has risen sharply in recent months, with one exception - precious metals - which have all the prerequisites to be next in line for a price rally.

Bull & Bear-Certificates

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.