Investing in China: sentiment is turning better?

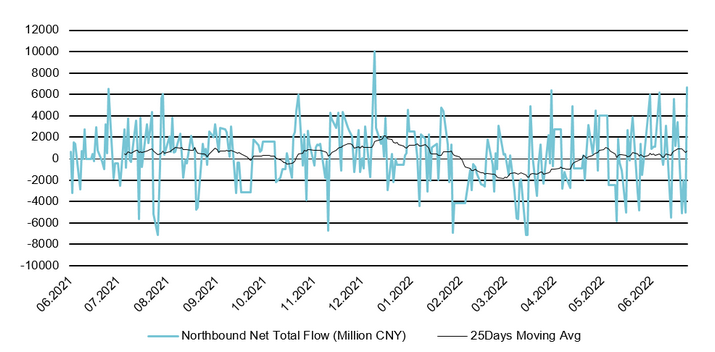

Chinese market is at inflection point. International institutions are gradually coming back to the Chinese equity market for diversification after sentiment is turning positive. Since beginning of May, the MSCI China has rallied 3% while S&P 500 lost 9.1% as of 22.06.2022. The northbound net total flow has turned positive i.e. net inflow, after the exodus of international investors in Q1.

Chinese market maybe at inflection point. International institutions are gradually coming back to the Chinese equity market for diversification after sentiment is turning positive. Since beginning of May, the MSCI China has rallied 3% while US S&P 500 lost 9.1% as of 22.06.2022. The northbound net total flow has turned positive i.e. net inflow, after the exodus of international investors in Q1, see Figure 1.

Investors are hunting for diversification. The inflation in major developed markets has been mounting to levels that have not been seen in decades. The Fed followed by other central banks announced possible acceleration on rate hikes to tame the inflation. Investors are speculating the factors driving inflation right now are not in control of central bank, i.e. Russia - Ukraine war and the application of strict zero covid rule in China. Aggressive rate hikes in combination with persistent high inflation could badly impact economy growth and lead to a recession. The market sell-off of the last months has affected several asset classes such as developed market equities, bonds, crypto currencies, making the correlation between different asset classes become rather positive. As a result of this, investors are rushing to find diversification to dampen the risk.

In contrast to major central banks, the People's Bank of China(PBoC) cut the five-year loan prime rate, a reference for mortgages, by 15 bps to 4.45% in May and it also released lending rules supporting small and micro business to make up for the economic damage of the zero COVID policy. As the gradual reopening of Shanghai in June continues, after two months strict lockdown, many investors believe that the worst time for investing in China has passed, expecting the government would gradually relax some of its Covid rules. Furthermore, more investors are inclined to believe that exposure to Chinese equity could add some diversification as the monetary policy of PBoC is diverging from major developed market central banks and the May inflation remains at 2.1% still below PBoC 3% target, while US inflation reached new high to 8.6%. The diversification with respect to the US market has also been demonstrated in the historical data in Figure 2: the Chinese equity market overall appears to have a rather low correlation with the US market with an average correlation of 0.12 and in the period of the the global financial crisis(GFC) the China Securities Index CSI 300 index shows a negative rolling correlation to S&P 500 index. In the recent months, the rolling correlation between the two markets has been falling rapidly to 0.08.

Consumers’ strength needs to be carefully observed. Despite a better investment sentiment, the risk from the government zero COVID rules should be carefully watched. China’s retail sales declined by 6.7% year-on-year in May and unemployment rate reached 5.9%, which is only marginally lower than the peak of 2020. The unemployment rate of the population aged 16 to 24 increases to 18.4% in April which sends worrying signal about the overall consumer health. Figure 3 shows that the lockdown affected the most consumer cyclicals, particularly automobile, and luxury goods, such as gold, silver and jewelry, but also garments and shoes while the demand for essential goods. but also for tobacco and liquor is rather resistant.

Adjustment in China new vision strategy. Based on the observation of the market conditions and given that the COVID rules would be still in play for an extended period, the Chinese consumer strength could be further squeezed. To take precautions, the portfolio target sector allocation in June is adjusted as following: reduce consumer discretionary by 5% to 30%, increase communication services by 1% to 16%, increase industrials by 1% to 6%, increase information technology by 2% to 14% and increase material by 1% to 3%.

Strategic Certificates

Risks

e

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the trading products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms. The base prospectus and final terms constitute the solely binding sales documents for the securities and are available under the product links. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future result.