Gold increasingly in focus, but diamonds lose their luster

Swedish economists have traditionally had a negative attitude towards gold. The metal is considered a relic in the financial market, which has meant that the Swedish Riksbank has lost many billions in selling the metal in recent decades. Is it time to buy now?

Swedish economists have traditionally had a negative attitude towards gold. The metal is considered a relic in the financial market, which has meant that the Swedish Riksbank has lost many billions in selling the metal in recent decades. Is it time to buy now?

The Swedish Riksbank is probably at the forefront of development of electronic currencies. The cash handling system is already disappearing in Sweden. The positive thing is, of course, that robberies are radically reduced in the trade. The downside is that society becomes less robust and that personal integrity in principle ceases. The authorities have a theoretical opportunity to subsequently track virtually all transactions and map an individual down to the lowest level. As a citizen of Sweden, you can of course choose to trust the good will of the authorities…

In our eyes, reasoning around gold is parallel to the debate concerning the Swedish defence. The Swedish defence was also considered a relic in the decades following the fall of the Berlin Wall. The defence does not return any money but is at a first impression just a heavy cost item. The two advantages of defence, are of course, that the country is not so easily attacked in a major conflict. The second argument, which is more diffuse and not as relevant in this context, is that Sweden has been at the forefront in many areas of technology as we have had our own world-class defence industry. But just as it takes decades to build a defence, it is just as difficult to establish a larger asset base in gold on the day when gold comes into play again.

The graph below shows the gold price over the last two decades:

The Swedish Riksbank was clearly influenced by the Bank of England around 2007 when there was a debate about the Riksbank divesting part of its gold reserve. According to Tomas Fischer, owner of Fischer Securities at that time, the Riksbank had already lost SEK 2 billion between 2005 and 2007 due to its divestment of gold. Since then, the price of gold has risen further. The two graphs below show the gold price in purple compared to the index for the ten-year US government bond as an orange line. It is followed by a similar comparison between the gold price and the index for the ten-year German government bond.

The Riksbank has instead rewarded the purchase of interesting bearing bonds. On paper, it is obviously better to own something that yields a dividend each year, than something just lies and collects dust in the basement.

If you look at the graph above, bonds have also risen in value. The supply has been large, but the demand even greater when the central banks buy up the bonds that the states push out in the market.

You might ask if gold is something that you as an investor should own. Our attitude is more that you should see gold as another investment and that you should have a share of gold in a diversified portfolio.

American super-investor Warren Buffett also seems to have changed his view of gold after having bought shares in the gold company Barrick Gold:

Since Warren Buffett has been a major critic of owning gold, this has attracted attention. Among other things, he has said that the purchase of gold is anti-American. Maybe that is why instead of buying gold directly, he takes the detour by buying shares in a gold company? Regardless, the exposure is about the same, as Barrick Gold is a good instrument for gold.

Link to Warren Buffett: https://www.marketwatch.com/story/did-warren-buffett-just-bet-against-the-us-economy-his-latest-investment-raises-some-questions-2020-08-16?mod=article_inline

Bull & Bear-Certificates

Gold has the most attraction in times of inflation, which is something that central banks have tried to create in recent decades without success. Falling prices for IT and China´s large contribution as the global low-cost factory has pushed down prices for the benefit of all. If, on the other hand, the central banks chose to include asset prices such as private housing and shares in the inflation measures, inflation, on the other hand, would look completely different. The large supply of capital seems to have driven down interest rates (and thus inflation) instead of driving up inflation as the current theory looks.

The main argument for gold is that people see it as a perfect means of payment and that gold is a finite asset. Seen from these perspectives, gold should have skyrocketed in value with the gigantic capital injections made in recent years by central banks by supporting the purchase of bonds in the market.

But from our perspective, this interest in gold has instead been sucked up by a gigantic apparatus of paper gold in the form of derivates and ETFs that has been pushed out in the market. These are not fully insured in physical gold but are only about commitments to deliver something, without 1:1 insurance in the physical raw material. This is a bubble that could eventually burst. If it does, it does not mean an escape from gold. On the contrary, security requirements should instead increase, which leads to a short squeeze in the market when issued promises are to materialize.

Like all other types of assets, gold is about timing. Interest varies over time. What we are seeing now is that the major gold buyers in the market- China and India- are reducing their purchases. With falling oil prices, one can also count on declining interest from Russia and the Arab countries, which have otherwise increased their holdings in recent years.

As can be seen from the picture above, especially India is selling net gold right now. Newspaper reports says that it is private individuals and entrepreneurs who sell in both India and China to cope with the Corona crisis. Around New Year, the interest from these buyers usually increases, so there are some interesting months ahead of us. For those who want to revel in data, we refer to this site (which of course is pro gold):

This is not the forum to go into depth on this issue. But all investors should take a stand on this issue themselves. For a Swedish investor it is important to understand that Swedish economists and asset managers in general have a clearly negative view of gold as an investment that we experience deviates from the international view.

Looking at the daily gold-graph below, one can see how the metal has peaked following an exponential rise and is now consolidating. The corresponding upturn and possible subsequent consolidation can, with a lag, now be seen on the stock market on Nasdaq and especially Apple. It looks like gold is trying to test upwards now but has break above both MA20 and MA50 before the previous top can be tested. However, a cautious increase in a gold position does not have to be wrong.

This can be a good period to build up gold holdings but both gold and gold stocks could continue to fall for a period. In the short term, this is said to be governed by the stock market. If shares fall, the gold is dragged down since correlations are so high between assets classes nowadays. If the stock market rises, so will gold.

The diamond price index as shown in the graph below, on the other hand, we are much more hesitant about. De Beer´s monopoly is slowly being relaxed by the emergence of increasingly high-quality industrial diamonds, which are pushing up prices from below. Natural diamonds will always defend their place, but slowly though for certain the quality of industrial diamonds will improve. This is a very strong force against any price increase in the market.

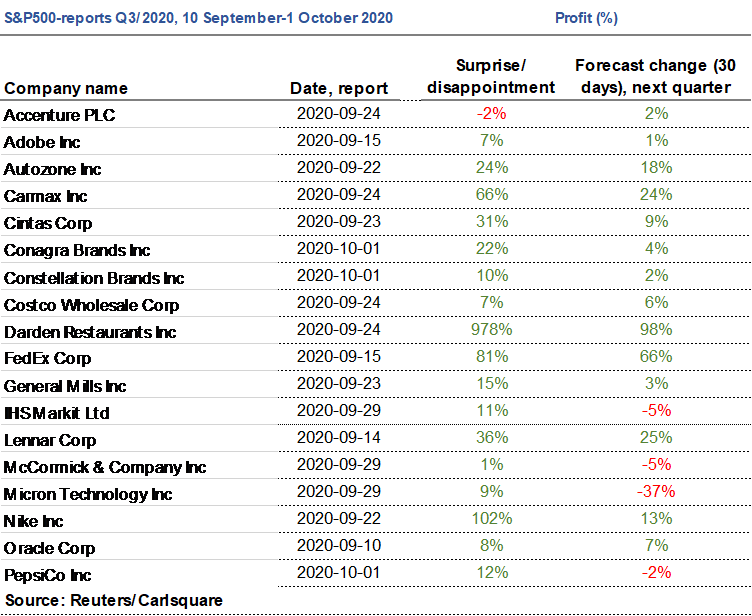

The Q3 reporting season

Only six S&P 500-companies have reported their Q3 figures (equivalent) in the past week. Thus, we are up in 18 of 506 companies that have reported their figures. The trend remains strong, 17 of these 18 companies have surprised the market positively in terms of profit outcome. It is a little less strong when we study the right-hand column, which is forecast change (30 days) for the next quarter. There, only 14 out of 18 are an upward revision, which, however, still means a clearly positive trend.

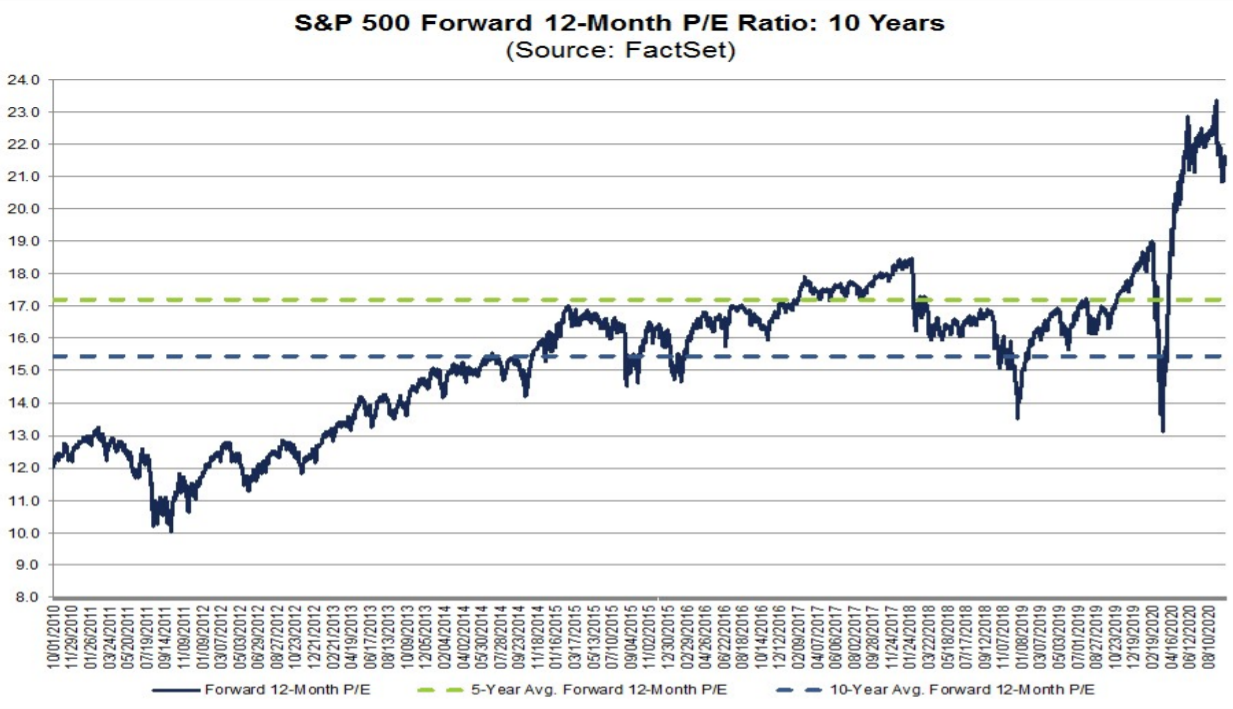

If we go on to the P/E-ratio valuation of the S&P 500 index, we can see that the P/E-ratio has increased from 12x in 2012 to gradually reaching a top of 23x a few weeks ago to fall back to just under 21x right now.

The stock markets are currently experiencing mild autumn chills. The graph above shows how the markets have begun to decline with oil-heavy Russia (Moscow Stock Exchange) at the forefront, followed by Covid-affected France. The S&P500 is in the middle segment following the recent downturn. At the top we find Germany (DAX) and Sweden (OMX). If this is due to belief that Sweden and Germany will do better than the United States due to Covid 19, then we believe that this might be the wrong conclusion. If, on the other hand, there is a reweighting between European portfolios, the development becomes more logical.

OMXS30 is still trading in a short rising trend. As seen in the graph below, the index fell below MA20 as well as the psychologically important 1 800-level on Friday intraday, but managed to close above. EMA9 still remains to be retaken before previous local tops around 1 845 can be tested:

The German DAX index looks significantly weaker but bounced nicely on MA100 on Friday. The next levels on the upside is EMA9 at 12 756, MA50 at 12 855 and MA20 at 12 922:

The S&P500 index is traded at a clear crossroads. Note how the MA values converge to the same point, which indicates a market in perfect balance. But the stock market is a trending market, which is why balance and consolidation are always followed by a trending period:

In the 2-hour graph, the S&P 500 broke out of its wedge-formation and reached the target price close to Fibonacci 50. Now note how MACD has generated a weak sell signal in the 2-hour graph:

Mini Futures

The moving averages are converging for Nasdaq in a similar matter to S&P 500:

In the 2-our graph for Nasdaq, MACD has generated a weak sell signal. However, media has over the weekend reported that Trump may be sent home from the hospital today, which may put some buy pressure on the market.

Apple shares bounced nicely on the rising trendline. Also note that MACD has generated a weak buy-signal, which is a clear stock-market positive signal:

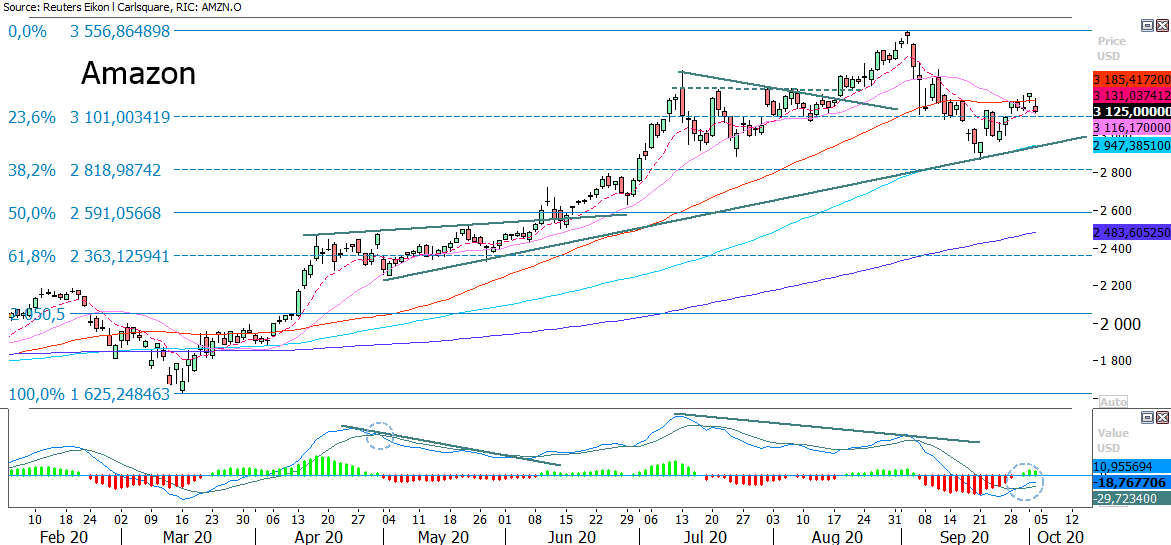

MACD has also generated a weak buy-signal in the Amazon stock:

The EUR/USD is consolidating along Fibonacci 23.6. MA20 is pushing the currency pair downwards from above. In case of a break to the downside, the next level can be found around 1.16 followed by MA100 at 1.153. On the upside, MA50 arounf 1.18 serves as a second resistance after MA20 at 1.176:

Oil (Brent) is under pressure and weighted by worries of a second wave of Covid 19. Can Fibonacci at 38.2 USD per barrel act as a magnet and support? Se graph below:

Bull & Bear-Certificates

Bitcoin is consolidating in a neutral wedge-formation. A break to the upside calls for a target price close to previous local top just below 12 485. A break to the downside and the formation’s target price is found around Fibonacci 38.2 at 9 192:

Risks

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.