Go long or short emerging markets currencies

Vontobel expands its leverage product offering on currencies. Up until now, the offering has been limited to the US Dollar, Great British Pound, Euro, Japanese Yen, Swedish Krona and Danish Krona. Through the new Mini Futures, investors will also be able to gain long or short exposure to the Turkish Lira, Russian Ruble and South African Rand, with leverage.

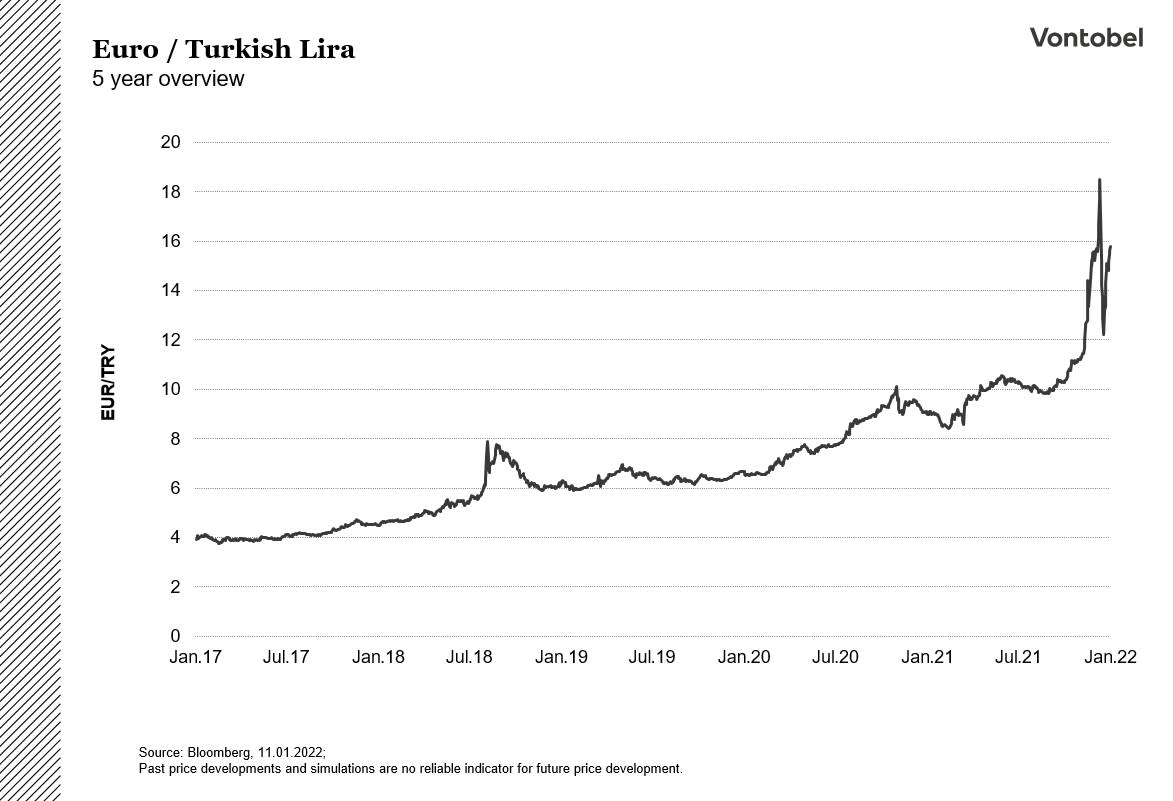

Turkish Lira

Recep Tayyip Erdogan, President of Turkey, has long defended low interest rates through a combination of religious and economic arguments that many economists deem contrary to mainstream economic theory. In an attempt to fuel growth and exports and increase employment, Erdogan and the Turkish central bank have continually slashed interest rates (500 basis points since September) despite of an already inflationary environment. Last month the annual inflation rate soared to 36.1% (the highest figure in two decades). Year-on-year, food and drink prices have gone up by 44%, and in December of 2021 alone, consumer prices rose by 13.58%.

The economic policies and proceeding turmoil led to the Turkish Lira depreciating 41.0% against the Euro in 2021 alone and has created an exodus from lira denominated accounts into gold and foreign currencies (which according to central bank data now account for more than half of local’s savings). In an effort to support the Lira and to reverse dollarization, Erdogan announced a support program on December 20th, 2021. The program intends to make up for the differential between interest on deposits and further currency depreciation, effectively transferring any losses from deposit holders to the Treasury and ultimately the taxpayer. With Erdogan so far not showing any signs of reversing his course, only the future can tell what is in store for the Turkish currency.

Link to all new EUR/TRY-products

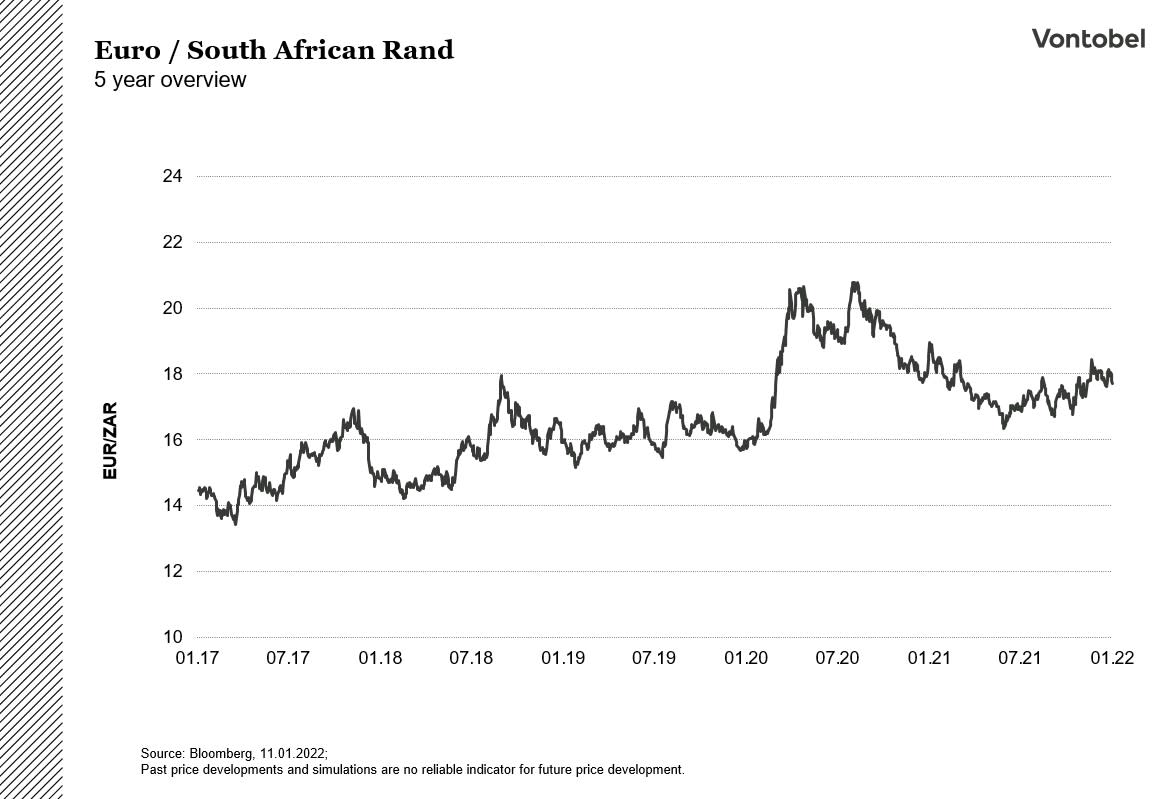

South African Rand

A net-oil importer, with gasoline accounting for roughly 5% of the nation’s inflation basket, South Africa is more sensitive to fluctuations in fuel prices than many other nations. With South Africa being the epicenter of the new Covid variant Omicron, and with high fuel prices potentially spreading across the South African economy, the task of balancing inflationary pressure and the recovery from the Covid-induced contraction has grown increasingly difficult for the South African central bank. The Rand is also highly susceptible to the Chinese economy (China being the largest importer of South African commodities) and to fluctuations in commodity prices. To date, South Africa has due to high commodity prices managed to maintain a current account surplus. A fall in commodity prices, or general slowdown in the Chinese economy amid further Covid concerns would likely put the Rand under increased pressure.

Link to all new EUR/ZAR-products

Russian Ruble

Although tens of thousands of Russian soldiers have been relocated to the Ukraine border, Vladimir Putin’s political intentions are still uncertain. A military invasion and the EU and US sanctions that would follow, would likely render any benefits from high commodity prices, large international reserves, and relatively low external debt irrelevant. An exclusion from international transaction networks and further limits on Russian banks would inflict harm on the Russian economy and could potentially render Russia “uninvestable”. An armed conflict is however still deemed unlikely by many observers.

While many other emerging market currencies have depreciated against the Dollar in the last year, the Russian Ruble has remained relatively stable. The Russian Central Bank recently raised the country’s key rate by 100 basis points to 8.5% (17.12.2021) in an attempt to mitigate rising consumer prices (rates were hiked 425 basis points in 2021). Investors should keep an eye on the development in energy prices and in how geopolitical events unfold.

Link to all new USD/RUB-products

Investing in emerging-market currencies

The development of emerging market currencies will in the foreseeable future largely be driven by how well the world manages to recover from the Covid-induced contraction, how geopolitical events unfold, and the development of energy prices. Through Vontobel’s new Mini Futures investors are provided with a vehicle for gaining exposure to three emerging market currencies or alternatively use them for hedging purposes. Investors can gain both long and short exposure with leverage, based on their individual conviction and risk preferences. Due to the leverage in the Mini Futures and the higher volatility of the underlying emerging market currencies investors in the products bear an increased risk of losses from their investment. The products are not capital-protected; hence a total loss of the investment is possible. Past performance of the relevant underlying instrument or currency pair is not a reliable indicator of future performance.

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the trading products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms. The base prospectus and final terms constitute the solely binding sales documents for the securities and are available under the product links. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities.