Blue horseshoe loves Occidental Petroleum

The news is marked by frightening war headlines, inflation threats, oil embargoes and interest rate hikes. The stock market has been rocking strongly this year. Most down. Many technology stocks have plummeted by 70-90% while oil companies have made a comeback. Is the rise of the last few days just a small so-called dead-cat bounce or maybe it is the beginning of a more significant bear market rally?

The news is marked by frightening war headlines, inflation threats, oil embargoes and interest rate hikes. The stock market has been rocking strongly this year. Most down. Many technology stocks have plummeted by 70-90% while oil companies have made a comeback. Is the rise of the last few days just a small so-called dead-cat bounce or maybe it is the beginning of a more significant bear market rally?

In any case, almost no one believes that the stock markets have bottomed out seriously and that today's prices would be a good opportunity to invest long-term. But, if you are still looking for inspiration for value-based stock purchases, where is a better place too look than Warren Buffett, the world's best investor of all time who in an almost legendary way has escaped the technology sector's recurring bubble cycles?

Right now, while his investment company Berkshire Hathaway owns almost half of the money (43%) in Apple, is Apple really a technology company? Or does Apple actually only sell simple consumer products like phones and entertainment?

In fact, Berkshire's holdings in traditional financial companies (26% of the portfolio) are more technology-heavy than Apple. Companies such as Bank America, American Express, Moody's, US Bancorp, Bank New York Mellon, Citigroup, VISA and MasterCard are based on much more impressive software, innovations and networks than Apple's sweatshops. If you disregard Apple's cult-like customer loyalty, it's probably much easier to develop products that compete side by side with phones and computers than with financial services.

Yes, it is true that about 70 percent of Berkshire's portfolio consists of only Apple + finance. It is obviously important to keep it simple, especially if you handle one of the world's largest and most well-known portfolios. Furthermore, soft drinks and ketchup stand out among the largest holdings.

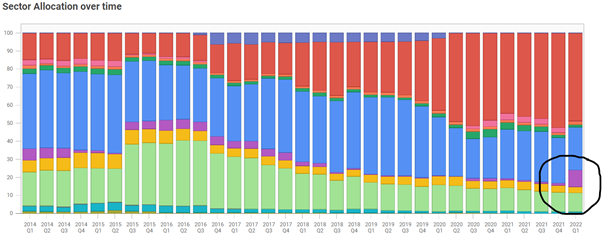

More interesting than what Buffett owns right now is what changes he has made lately. That is what will build wealth in the future. Berkshire is like a supertanker, it's not something you turn on a penny. Therefore, one should keep track of new trends in the portfolio.

At the top of the graph below you can see how Berkshire dipped its toes in the transport sector 2016-2019 but pretty soon chose to release it. Otherwise, the clearest development is the choice to let technology stocks (red bars) go from 10 to 50 percent, completely dominated by Apple of course but also some other companies. At the same time, consumer companies (light green) have decreased from 36% to 10%.

Most interesting of all, however, is the bite on energy (purple) where the portfolio weight from one quarter to another has gone from 1% to almost 10% through massive acquisitions of the companies Chevron and Occidental. Personally, I prefer ConocoPhillips in the sector, preferably supplemented with the system and service provider Schlumberger, but maybe the latter will start to get a little too expensive after all. The exact choice of company is a matter of detail. The important thing is that Buffett has concluded that in the long run it is time for a comeback for the energy sector. It now constitutes an unreasonably small share of the stock market's market value, given that energy is in short supply and underpins all economic activity. The companies have low Price / Earning ratios and have not kept up with the oil price, despite the fact that even higher oil prices are more likely than they would suddenly fall again. Russia's recent geopolitical aggressions, combined with ESG policies leading to low investment in the oil sector, guarantee oil shortages and continued high prices. Low valuation multiples are also extra attractive in a world with high inflation and rising interest rates, especially as the real asset oil has a built-in inflation protection.

The question is whether Buffett, at the same time as increasing holdings in the energy sector, will do something for Apple, because Berkshire's cash level is at the bottom of the range for the past 10 years. $ 39 billion goes a long way in itself, so there is hardly any acute shortage of liquidity. Apple's share is hardly cheap at over 6 times sales and 24 times profits, despite an expected growth of only 5-10% per year. This assessment applies in particular to the outlook for rising interest rates and increasing competition in all of Apple's core areas. On the other hand, Apple has repeatedly demonstrated the ability to use its strong brand to expand its business.

I therefore believe, after all, that Buffett stays with Apple. As with companies such as Coca Cola, Kraft Heinz and American Express, he has found simple companies with strong management and long-term proven business ideas. Apple really belongs there and so do several of the big oil companies. Historically, Berkshire has shown tremendous perseverance when it comes to the big bets in the portfolio and this is hardly an exception given that it ticks all the boxes in the long-term value investor's list of key criteria. I wonder if you shouldn’t speculate about some really big corporate deals in the oil sector as well. This is exactly what usually happens in resource companies at this stage of the commodity cycle.

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.